In 2020, the U.S. Department of Health and Human Services (HHS) decided that funds expended under the Provider Relief Fund (PRF) program, which at the time was the second largest federal program established by the Coronavirus Preparedness and Response Supplemental Appropriations Act, will be subject to a single audit or a financial audit. HHS subsequently clarified the types of audits available to for-profit entities, as further described herein.

This Snapshot provides certain updates and reminders related to PRF audit and reporting requirements.

Non-federal entities

The Addendum to the 2020 Compliance Supplement, issued in December 2020, announced that PRF expenditures and lost revenue would not be reported on the Schedule of Expenditures of Federal Awards (SEFA) or audited under the Office of Management and Budget’s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance) until Dec. 31, 2020 fiscal year-ends (FYEs) and later.

However, HHS did not open the PRF reporting portal for submissions of reports on PRF funds until July 2021. Due to the late launch of the portal, HHS pushed back PRF single audit requirements to fiscal years ending no earlier than June 30, 2021 for non-federal (not-for-profit and governmental) entities.

The 2021 Compliance Supplement reiterated that PRF expenditures and lost revenues will be included on the SEFA for FYEs ending on or after June 30, 2021 (and not before). The Appendix herein provides a summary of SEFA (or HHS awards) reporting of PRF for FYEs covered by the Post Payment Notice of Reporting Requirements published to the PRF reporting portal.

For-profit entities

While a for-profit entity may choose the type of audit performed, as described below, it is believed that a financial audit will be the most common. In that case, the Schedule of HHS Awards may be prepared in accordance with U.S. GAAP or a special purpose framework, such as the cash or tax basis of accounting.

Further, PRF revenue reported on the Schedule of HHS Awards comes from activity reported in the PRF reporting portal, and reporting in the PRF reporting portal is based on when PRF funding was originally received (not expended). The Schedule of HHS Awards is based on revenue recognized under different HHS programs:

- PRF program – Both eligible expenditures and lost revenues are conditions for earning and recognizing PRF revenue.

- COVID-19 Claims Reimbursement for the Uninsured Program and the COVID-19 Coverage Assistance Funds (Uninsured Program) (Assistance Listing 93.461) – Fees for service revenue is recognized during the period under audit.

- Other HHS programs – Revenue is generally equal to expenditures during the period under audit.

Multiple years of funding may be presented on the Schedule of HHS Awards, as illustrated in the Appendix. If funding is received from another HHS program, such as the Uninsured Program, the entity would follow the reporting requirements of that program to determine in which FYE to include such funding on the Schedule of HHS Awards, as previously summarized.

Reporting grace period for non-federal and for-profit entities

In March 2021, the Office of Management and Budget issued a memorandum to allow recipients and subrecipients with FYEs through June 30, 2021 that had not yet filed their single audits with the Federal Audit Clearinghouse as of the date of the memorandum to delay the completion and submission of the Single Audit reporting package up to six months beyond the normal due date. Then, in October 2021, the Health Resources and Services Administration (HRSA), an agency of HHS, granted the same extension to for-profit entities.

In October 2021, HRSA also announced a 60-day reporting grace period for both non-federal and for-profit recipients of PRF funding, with a submission deadline of Sept. 30, 2021 (Reporting Period 1). The deadline itself was not changed, and late reports will be considered out of compliance; however, a failure to meet the Reporting Period 1 deadline will not result in enforcement actions or single audit findings if entities are brought into compliance by the end of the grace period on Nov. 30, 2021. Deadlines for Reporting Periods 2-4 outlined in the Appendix were unchanged.

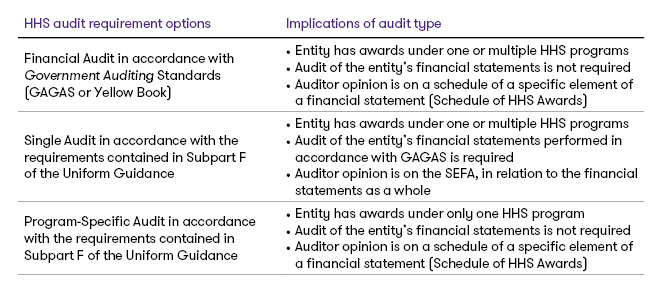

For-profit entity audit requirements

For-profit recipients that expend $750,000 or more of HHS awards, including PRF funds, during their fiscal year can elect one of the three options outlined in the table below to meet HHS audit requirements. Unless specifically excluded, all HHS awards are subject to the HHS for-profit audit requirements.

Examples of other HHS Assistance Listings include COVID-19 Claims Reimbursement for the Uninsured Program and the COVID-19 Coverage Assistance Funds (Assistance Listing 93.461), and COVID-19 Testing and Mitigation for Rural Health Clinics (Assistance Listing 93.697). Medicare is specifically excluded from the HHS for-profit audit requirement.

Any awards from other federal agencies are not included in the calculation to determine whether an HHS audit is required; therefore, the option described below to elect a single audit would only include HHS programs. If a for-profit entity receives funding from other federal agencies, the entity follows the audit requirements of those agencies.

Other guidance

HHS has published (PDF - 377KB) several FAQs on the PRF program. The FAQs cover a wide variety of topics, including general overview questions, terms and conditions for recipients, and auditing and reporting requirements. Some of the key questions and updates made relate to the following topics:

- The types of expenses that would be permissible uses of PRF distributions; in particular, the FAQs indicate that “The term ‘lost revenues that are attributable to coronavirus’ means any revenue that you as a health care provider lost due to coronavirus”

- Changes to reporting deadlines

- New fact sheets on independent audit requirements and parent-subsidiary reporting

- The anticipated submission extension for commercial organizations; a six-month extension was granted beyond the normal due date

- Using different lost revenue methodologies in different reporting periods.

Additionally, the AICPA’s Governmental Audit Quality Center is expected to release a practice aid in the coming weeks that will include FAQs, illustrative schedules, notes, auditor reports, and a primer on GAGAS.

The firm will continue to monitor the situation. The firm currently serves many clients in the CARES Act and Federal Emergency Management Agency (FEMA) funding areas, and our Public Sector practice works with the federal agencies that administer these funds.

Appendix

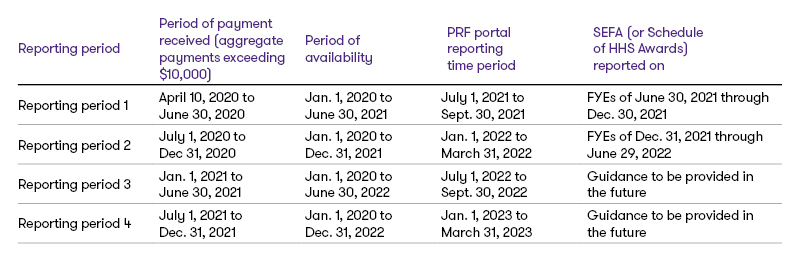

Reporting requirements for PRF recipients are outlined in a Post Payment Notice of Reporting Requirements published to the PRF reporting portal on June 11, 2021, which supersedes a previous version released on January 15, 2021. The notice states that recipients of PRF funding are required to report these funds as part of the post-payment reporting process; recipients who received one or more payments exceeding $10,000 in the aggregate during a “Period of payment received” are required to report in each applicable “Reporting period,” as shown in the following table.

PRF activity reported on the SEFA (or Schedule of HHS Awards) comes from activity reported in the PRF reporting portal, and reporting in the PRF reporting portal is based on when PRF funding was originally received (not expended). The following table outlines the relationship between the timing of payments received, used, and reported.

Download a printer-friendly version here: Provider Relief Fund updates and reminders (PDF - 307.39KB)

Contacts:

Partner, National Professional Standards

Partner, Audit Services, Grant Thornton LLP

Partner, Grant Thornton Advisors LLC

Flo Ostrum is the national professional practice director for the Government Audit and Not-for-Profit Audit Services practices. She brings over 25 years of experience working in the government and not-for-profit sectors to clients and engagement teams across the firm.

Fort Lauderdale, Florida

Industries

- Manufacturing, Transportation & Distribution

- Not-for-profit & Higher Education

Service Experience

- Audit & Assurance Services

Partner, Audit Services, Grant Thornton LLP

Partner, Grant Thornton Advisors LLC

Mike Sorelle is an Audit Services partner and the Atlantic Coast market territory Health Care practice leader. He is based in the Philadelphia office and also serves on Grant Thornton’s national Health Care leadership team.

Philadelphia, Pennsylvania

Industries

- Healthcare

- Not-for-profit & Higher Education

Service Experience

- Audit & Assurance Services

- Tax Services

- Advisory Services

- Financial Modernization

- Operations and Performance

- Commercial and Growth

- Alliances

- Technology Modernization

- Growth and transformation

- Valuation and Modeling

- Cybersecurity and Privacy

- Accounting Advisory

- Private company audit

- Transaction Advisory

Partner, Technology Modernization

Grant Thornton Advisors LLC

David has 30 years of experience primarily in the health system and health plan areas.

This Grant Thornton LLP content provides information and comments on current issues and developments. It is not a comprehensive analysis of the subject matter covered. It is not, and should not be construed as, accounting, legal, tax, or professional advice provided by Grant Thornton LLP. All relevant facts and circumstances, including the pertinent authoritative literature, need to be considered to arrive at conclusions that comply with matters addressed in this content.

For additional information on topics covered in this content, contact a Grant Thornton LLP professional.

Trending topics

Share with your network

Share