Finance leaders expect growth but worry about costs

Even as indicators of a potential recession continue to flare, more than half (53%) of finance leaders are optimistic about the economy, according to Grant Thornton LLP’s CFO survey for the first quarter of 2023.

The portion of CFOs who project a rise in net profits for their organizations over the next 12 months is rising and eclipsed two-thirds of respondents in the newest survey. And their concerns about the availability of materials in their supply chains and workers in their labor pools are easing.

Optimism is tinged with concerns

Although CFOs seem largely optimistic, there’s a caveat to this survey’s results. The latest survey was in the field in early March, prior to the Silicon Valley Bank and Signature Bank collapses that caused turmoil particularly in the financial services and technology industries. Any negative vibes resulting from the banking sector turbulence over the last several weeks were therefore not captured in this survey.

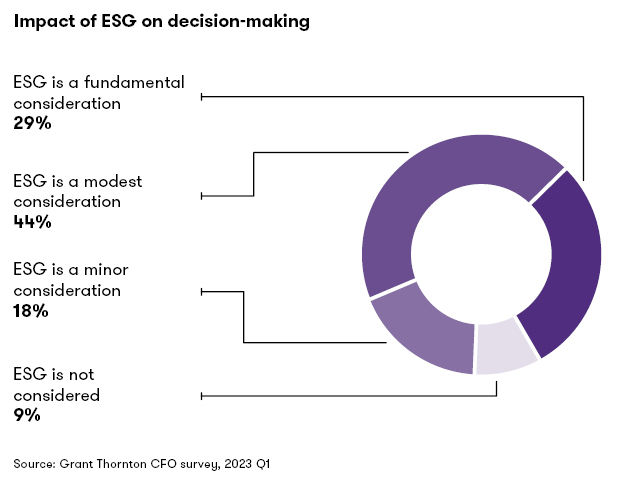

With the SEC expected to issue new climate disclosure requirements in the first half of this year, the survey sought to understand how CFOs are handling environmental, social and governance (ESG) topics and reporting in their organizations. Finance leaders reported that they are taking stock of ESG in their strategic moves and preparing to report their ESG metrics in a thorough fashion. Almost three-fourths (73%) of CFOs give at least moderate consideration to ESG when they’re making decisions, and more than half have clearly defined ESG goals and already report progress against ESG key performance indicators across all applicable geographies.

As spring commences in the northern hemisphere, CFOs are watering the flowers in expectation of growth, but they’re also battling the weeds. Cost optimization remains their top area of focus, and those who feel confident in their ability to meet organizational goals for controlling costs fell 9 percentage points from the previous quarter to 50%.

“Some companies are reviewing all their contracts and relationships to see where they might have opportunities to save on costs,” said Sean Denham, National Audit Growth Leader for Grant Thornton.

So the outlook for the rest of the year is mixed. In short, CFOs are expecting a bumpy ride as the year develops, but they’re buckling in and driving forward with the idea that the road will get smoother later in the year.

“Some companies are reviewing all their contracts and relationships to see where they might have opportunities to save on costs.”

Cost control remains a priority

For the fourth straight quarter, CFOs ranked cost optimization as their top area of focus.

This may be partly due to a challenging economy and partly due to CFOs’ role as the penultimate financial stewards at their organizations.

“The economy is up and down, and people are probably trying to hedge a bit to make sure that they're not going to overspend,” said Lisa Heacock, Partner of Finance Transformation for Grant Thornton. “It's just hard to get that balance. I do think it's a combination of the environment as well as just being proactive in looking at expenses.”

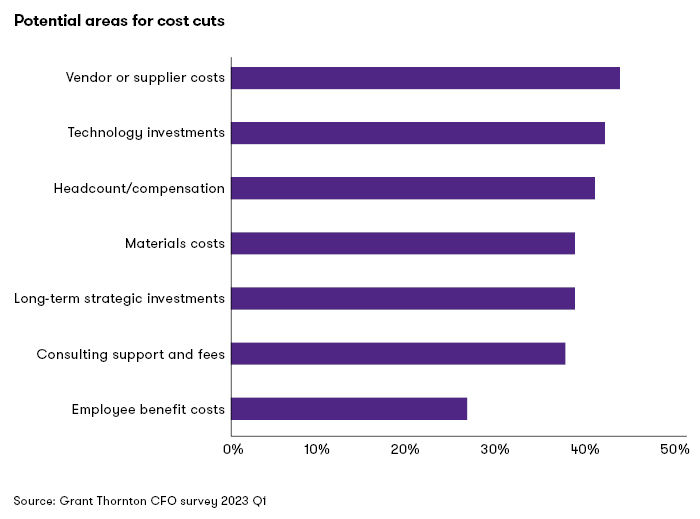

What might CFOs be looking to cut? Technology spending experienced a double-digit increase as an area for possible cuts. Vendor and supplier costs were the top area of potential cuts for CFOs, and materials costs saw a double-digit rise as an area for cost cuts compared with six months ago, perhaps because supply chain woes are easing.

“No matter what, CFOs should be looking and always figuring out ways to consolidate and get the most bang for the buck with their service providers and vendors.”

Heacock said CFOs should constantly be looking to their procurement and sourcing functions for potential savings. For example, if they have four different cell phone vendors throughout their company, they should consider consolidating into one deal with one vendor, using the volume to negotiate a more favorable deal.

Denham said that in a difficult economy CFOs start making sure they can fund the organization’s needs and scaling back where necessary on things they want. Similarly, Heacock said finance leaders might choose to eliminate some of the “nice-to-have” items on their wish lists.

“No matter what, CFOs should be looking and always figuring out ways to consolidate and get the most bang for the buck with their service providers and vendors,” she said.

Emphasis on strategy and reporting

When the SEC issues its long-awaited climate disclosure requirements, it’s expected that they will affect both the public companies that the SEC regulates and the companies that do business with them.

The survey shows that respondents are gearing up for that reporting. More than one-fourth (27%) of CFOs said ESG disclosures will be one of the biggest challenges their business will face over the next six months. That’s more than double the percentage from the 2022 Q3 survey.

While it would be a stretch to say that ESG is top-of-mind for most companies, as other challenges were rated as more significant than ESG reporting, ESG nonetheless is a significant factor in strategic discussions for many CFOs. More than one-quarter (29%) said ESG is a fundamental consideration in their decisions, while an additional 44% said ESG is a moderate factor in decision-making. Just 9% don’t consider ESG at all.

Meanwhile, regulatory compliance is hardly the only factor causing CFOs to act on ESG initiatives. They also get substantial benefits from implementing ESG considerations into their operations. One of the biggest benefits is an enhanced reputation. More than half (56%) of respondents said improving the reputation of their brand is a benefit of an enhanced ESG program.

“There’s clear research that shows the value of reputation for a publicly traded company is more than its financials and physical assets combined,” said John Friedman, Managing Director, ESG & Sustainability Services for Grant Thornton. “That’s a flip since the 1970s. Now it’s understood just how much your reputation affects your valuation.”

CFOs’ sense of ESG’s impact on reputation is apparent in their increasing perception that it’s an important topic to their customers as well. In the third quarter of 2021, 28% of CFOs cited customers among the stakeholder groups that are motivating them to enhance their ESG programs. That figure rose to 39% in the current survey.

Meanwhile, the desires of executive management (44%) and employees (43%) are the top factors motivating finance leaders to take action on ESG. Members of Grant Thornton’s ESG practice say it’s important to remember that any action on ESG will appeal to multiple stakeholder groups at the same time, particularly younger people who have the potential to be employees as well as customers in a labor market that remains tight in some industries.

“Companies can get overwhelmed trying to address each stakeholder group’s expectations individually, but if instead they focus on proactively identifying the ESG areas where they can have a meaningful impact, they can address many stakeholders at once,” said Jessica Feeley, Director, ESG & Sustainability for Grant Thornton. “If something is important to employees, it’s probably important to some degree to customers and the board too. If you focus on quality and you're able to move the needle even on one ESG initiative, you can have an impact across all those different groups at once.”

“There’s clear research that shows the value of reputation for a publicly traded company is more than its physical and financial assets.”

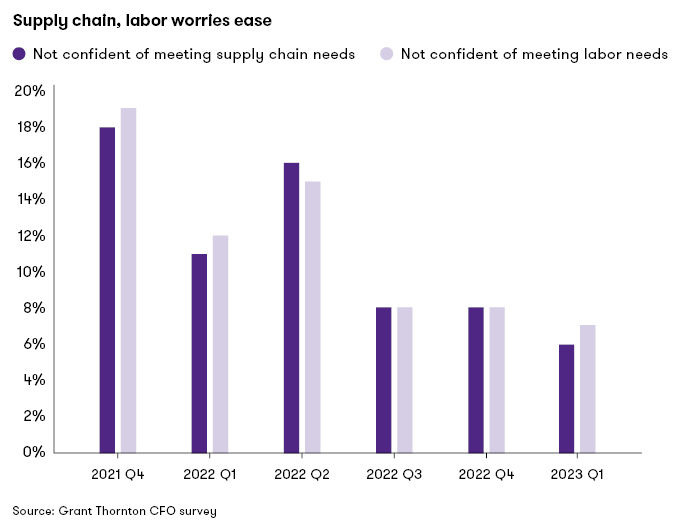

Supply chain and labor pressures diminish for some

Since the early stages of the COVID-19 pandemic, CFOs have faced significant challenges with supply chains and labor availability.

Pandemic-related shutdowns in factories and ports sent finance leaders scrambling to find new sources for goods, even as they implemented technological solutions to improve their supply chain processes. And after pandemic-fueled layoffs and furloughs were followed by the Great Resignation, companies in many sectors struggled to hire enough people to keep their operations running smoothly.

The latest CFO survey shows that those challenges are easing slightly. For the first time since the second quarter of 2022, finance leaders did not rate supply chain as their biggest challenge.

Meanwhile, 55% of respondents said they are confident in their ability to meet supply chain needs — the highest percentage since Grant Thornton began asking the question in the fourth quarter of 2021.

At the same time, the portion of CFOs who are not confident that they can meet their labor needs plummeted to 7%, an all-time low in the survey. The labor situation varies substantially based on industry, though, as many technology and media and entertainment industry companies have recently announced layoffs while many healthcare and manufacturing companies continue to struggle to fill their open roles.

Some companies even have found they’ve laid off too many people and are having difficulty getting important work done.

“They need to backfill positions and they can’t find anybody,” Heacock said. “So there’s no single answer as far as human capital spend. It just depends on the industry, the maturity of the organization and their finance operating model.”

Forty-two percent of CFOs noted headcount and compensation as an area to potentially cut costs — that’s an increase of seven percentage points from the previous quarter. But it’s safe to say that employment is a mixed bag depending on industry and other factors, whereas early last year, seemingly every company was suffering from some sort of worker shortage.

CFOs lead on strategy and ESG

In an environment with substantial opportunities and many risks, leading CFOs are continuing to partner with the rest of the leadership team and the board to find the balance between cost-cutting and investing for short-term gains and long-term growth.

More than any other person in the organization, the CFO typically has access to the appropriate financial and business data to inform decision-making. Leading CFOs are exploring technology investments, creating efficiencies, finding ways to source lower-cost resources and mitigating risks associated with talent and the workforce.

With regard to ESG, CFOs are helping organizations define their own approach to strategy, operations and reporting to enable compliance and meet internal and external expectations.

None of this is easy, but the optimism reflected in the survey for the first quarter shows that CFOs have confidence in their ability to push their organizations forward even in the present conditions.

How GT can help

ESG services

Finance transformation services

Contacts:

National Tax Leader, Corporate Tax Solutions

Grant Thornton Advisors LLC

Chris Schenkenberg has extensive experience working in M&A, conducting tax due diligence reviews for both financial and strategic clients. He also has significant technical knowledge in acquisition structuring, divestiture planning and tax accounting methodologies.

Chicago, Illinois

Industries

- Manufacturing, Transportation & Distribution

- Technology, Media & Telecommunications

- Retail & Consumer Brands

Service Experience

- Tax Services

Boston, Massachusetts

Trending topics

No Results Found. Please search again using different keywords and/or filters.

Share with your network

Share